Crypto M&A: Barbarians on the Blockchain

Sunday, November 24, 2019Crypto M&A – A comprehensive review

Crypto M&A is alive and kicking. 350 acquisitions involving cryptocurrency and blockchain companies have taken place since 2013. However, beyond anecdotes, press releases and high level summaries, there haven’t been any thorough or forward-looking analyses, until now.

What follows is a condensed version of a full research report that can be downloaded for free:

Enter email to receive a link to download the full report

Deal Activity

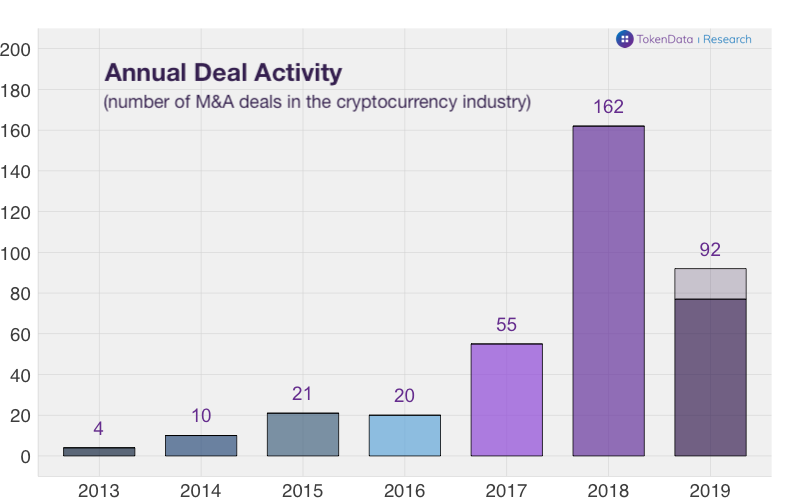

350 acquisitions involving cryptocurrency and blockchain companies have taken place since 2013. M&A activity peaked in 2018 with more than 160 deals, and we estimate 90-100 deals for 2019.

M&A activity is volatile and seems positively correlated to crypto prices and industry sentiment. Monthly activity peaked in early 2018 as prices and industry attention soared.

Deal Value

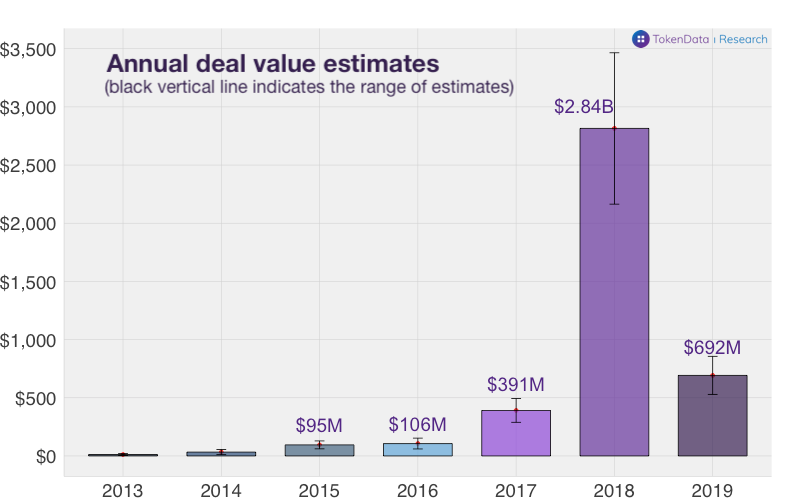

We estimate total deal value at $4 Billion since 2013, with $2.8B of M&A activity in 2018 and $700M in 2019. These figures might sound impressive, but are small compared to the total network valuation of cryptocurrency networks ($200B+). This makes sense given the early stage of this industry: most companies are less than 5 years old and a significant IPO seems years away.

A closer look at marquee transactions and interesting deals shows only one $100M+ transaction in 2019, versus five in 2018. However, 2019 has seen interesting acquisitions such as the acquisitions by Facebook for its Libra project, the consolidation in the crypto custody space (Coinbase-Xapo custody) and the first token merger.

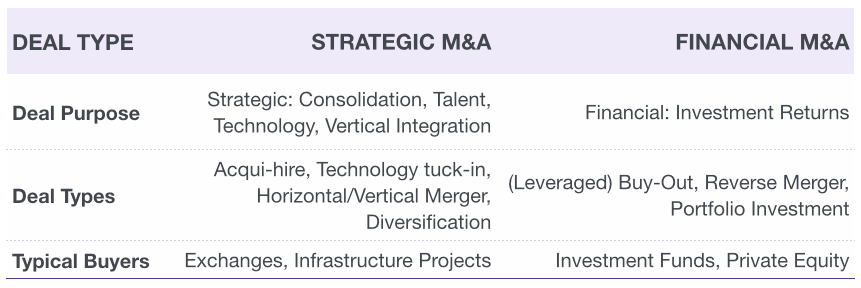

Financial vs Strategic: Not all M&A is created equally

We can split deal activity into two categories: Financial and Strategic M&A (description in table).

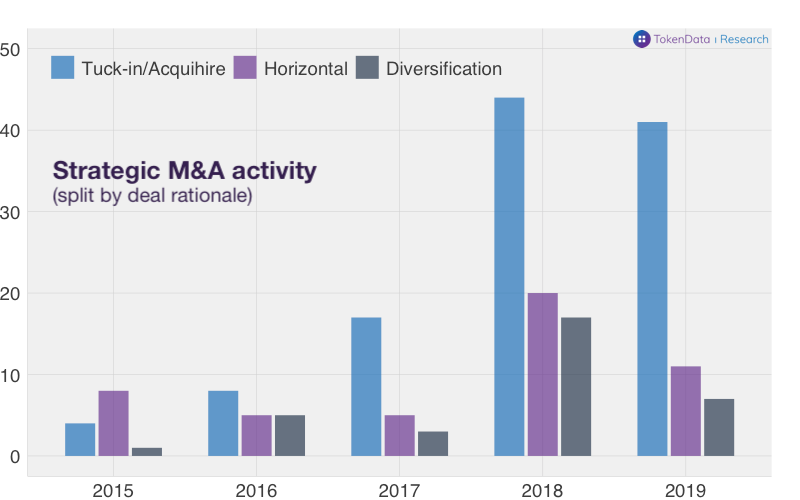

2018: Financial M&A with obscure motives. As shown in the graph below, Financial M&A outpaced Strategic M&A in 2017 and matched it in 2018. A closer look at the Financial M&A activity shows that many acquisitions consisted of a) defunct non-crypto companies turning into crypto investment companies (e.g. Long Island Blockchain) by acquiring small cryptocurrency startups and b) reverse mergers, in which private crypto companies acquired listed shell-companies.

2019: Strategic M&A continues its strength. The opportunistic and sometimes obscure Financial M&A disappeared during the market correction in 2018 and has been absent in 2019. Strategic M&A has held up well, with a projected 70 deals for 2019.

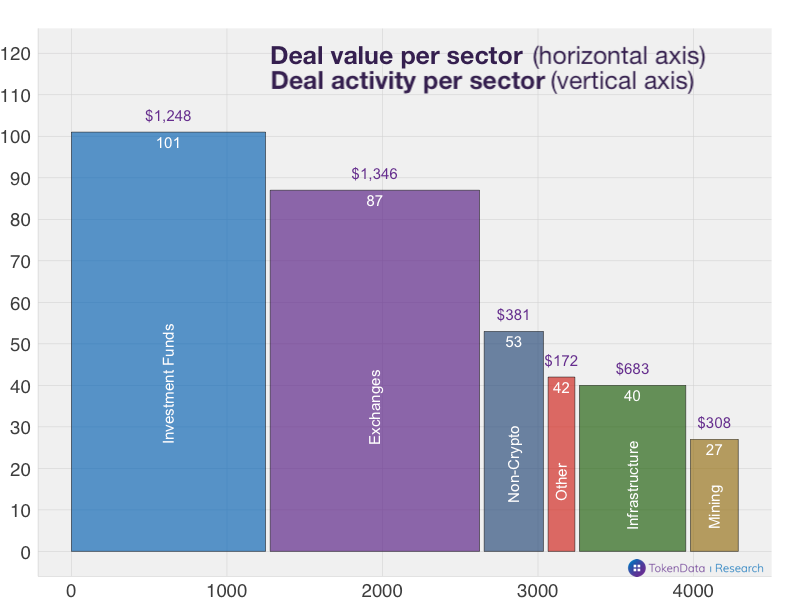

Sectors: Funds & exchanges in the front seat of acquisitions

>50% of M&A is done by investment funds and exchanges: Investment funds and cryptocurrency exchanges are the most active acquirers. Combined, they represent more than half of all deal activity and deal value.

Exchanges as prolific strategic buyers: Trading and speculation are crypto’s first killer-app, giving exchanges the necessary cash reserves and networks to engage in acquisitions.

“Pay to Play”: Non-crypto companies have been acquiring cryptocurrency startups to increase their industry presence. The majority of these acquisitions are talent-focused acquihires. For example, Facebook has acquired two startups (Chainspace & Servicefriend) for its Libra and Calibra development efforts.

Crypto Infrastructure & Mining: Crypto infrastructure companies and development teams of protocols and decentralized applications (dapps) have also been active, with 40 acquisitions. Mining companies were very active before the market correction in 2018, but have been largely absent in 2019.

Exchanges: Coinbase is the M&A powerhouse

Exchanges and trading-related companies are the most active strategic buyers. But which companies are the active dealmakers in the space?

Coinbase is the leader in Strategic M&A with 16 acquisitions. While the company’s M&A strategy mainly consists of acquihires and technology “tuck-ins”, it has also engaged in two significant acquisitions such as Earn ($100M) and Xapo’s custody business ($55M).

Kraken and Coinsquare follow Coinbase, with Kraken involved in 7 deals and Coinsquare in 5 deals. A significant transaction was Kraken’s $100M acquisition of Cryptofacilities, a regulated cryptocurrency derivatives exchange based in the UK.

Where’s Binance? Despite its size, growth and breadth of offerings, Binance has engaged in “only” 3 public acquisitions (Trustwallet, JEX, Wazirx) so far. However, Binance does have significant investments in other crypto companies and partnerships that have the same strategic effects as M&A.

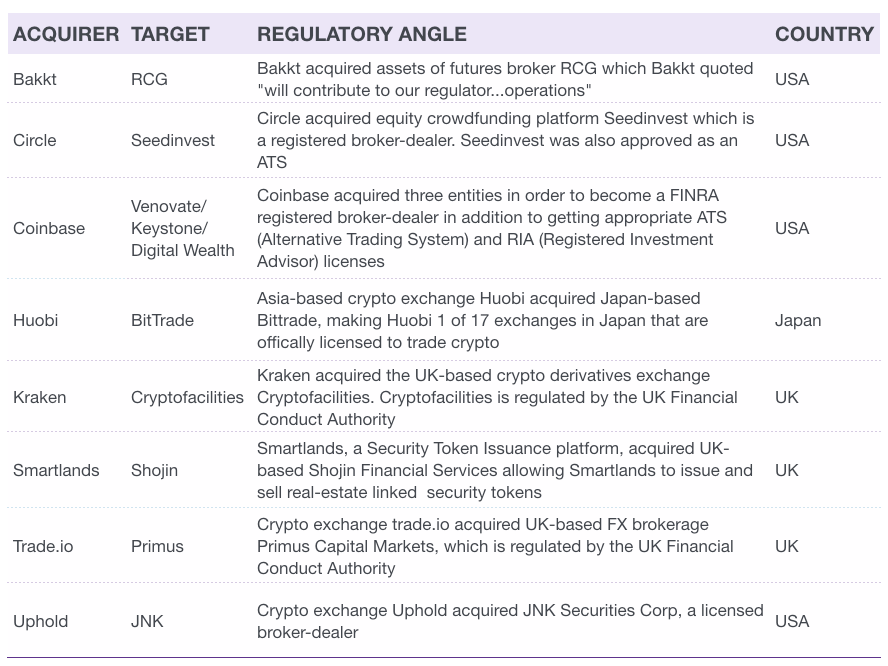

M&A as a way to overcome regulatory hurdles: M&A is used by cryptocurrency exchanges as a strategic tool to gain regulatory approval in certain jurisdictions or for certain products. They do so by acquiring a company which has the relevant regulatory licenses. We count 15 deals (some examples below) that have taken place since 2018 and explicitly mention regulation as an important aspect of the acquisition in their announcements.

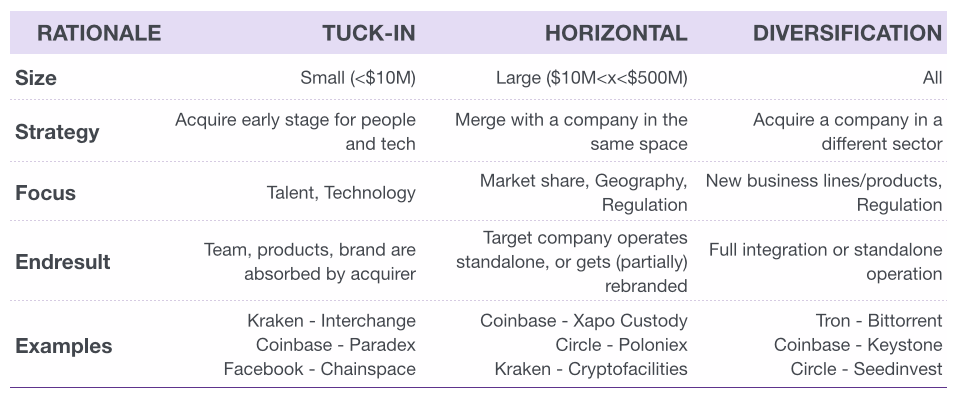

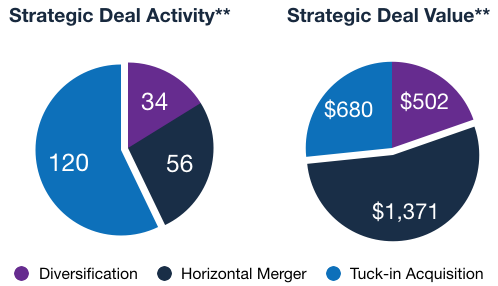

Acquihires & Technology Tuck-ins drive strategic M&A activity

To understand the rationale of each acquisition we have categorized all acquisitions into three different strategic types.

Talent & Technology Tuck-Ins* are the most common type of strategic M&A within the cryptocurrency industry and have been steady throughout 2018 and 2019. The focus on acquihires and early-stage technology acquisitions suits nascent industries.

*We use the term as coined by Coinbase COO Emilie Choi in various interviews on M&A in the space:

https://www.theblockcrypto.com/post/25055/emilie-choi-coinbase https://www.businessinsider.com/coinbase-crypto-bitcoin-acquisition-strategy-emilie-choi-2018-4?international=true&r=US&IR=T

Horizontal mergers represent only a quarter of all strategic deal activity. However, they make up more than half of strategic deal value as they typically represent the consolidation of larger and more mature businesses.

Diversification deals are a mixed bag. Within this category fall acquisitions in which crypto companies acquire traditional financial institutions for their regulatory licenses (e.g. Coinbase, Bakkt, Kraken) and acquisitions in which cryptocurrency protocols acquire non-crypto companies for their existing user base (e.g. Tron and Bittorrent).

Decentralized M&A

The analysis so far has focused on concepts that are common in “traditional” finance and the merger of centralized companies. In this section we look at how cryptocurrency networks can merge. A handful of thought pieces* have theorized what mergers of decentralized cryptocurrency networks might look like and the questions that arise. For example: how would a merger of two competing privacy cryptocurrencies take shape? Or how can a decentralized prediction market launch a hostile takeover of a competitor? Unsurprisingly – this pure form of “Decentralized M&A” hasn’t happened yet, as many cryptocurrency networks are still early in their development and run by centralized companies and foundations.

Decentralized M&A Thought Pieces:

“Protocol M&A” by Ryan Selkis

“What the First Token Hostile Takeover Could Look Like” by Andy Bromberg

“ICO M&A? Token Exits Could Get Messy” by Ash Egan

Crypto-native M&A concepts: However, as the current batch of cryptocurrency networks and blockchain projects mature – and the degree of decentralization increases – new stakeholders, concepts and mechanisms will appear in the M&A process. We have summarized a few concepts and mechanisms of “Traditional M&A” and speculated about their crypto-native or “Decentralized M&A” counterparts.

Live experiments: In addition, we are seeing some attempts to put theory into practice, as evidenced by the M&A activity by development teams and exchange of tokens instead of equity and/or cash. We look at these examples in the next sections.

M&A by protocol and dapp projects

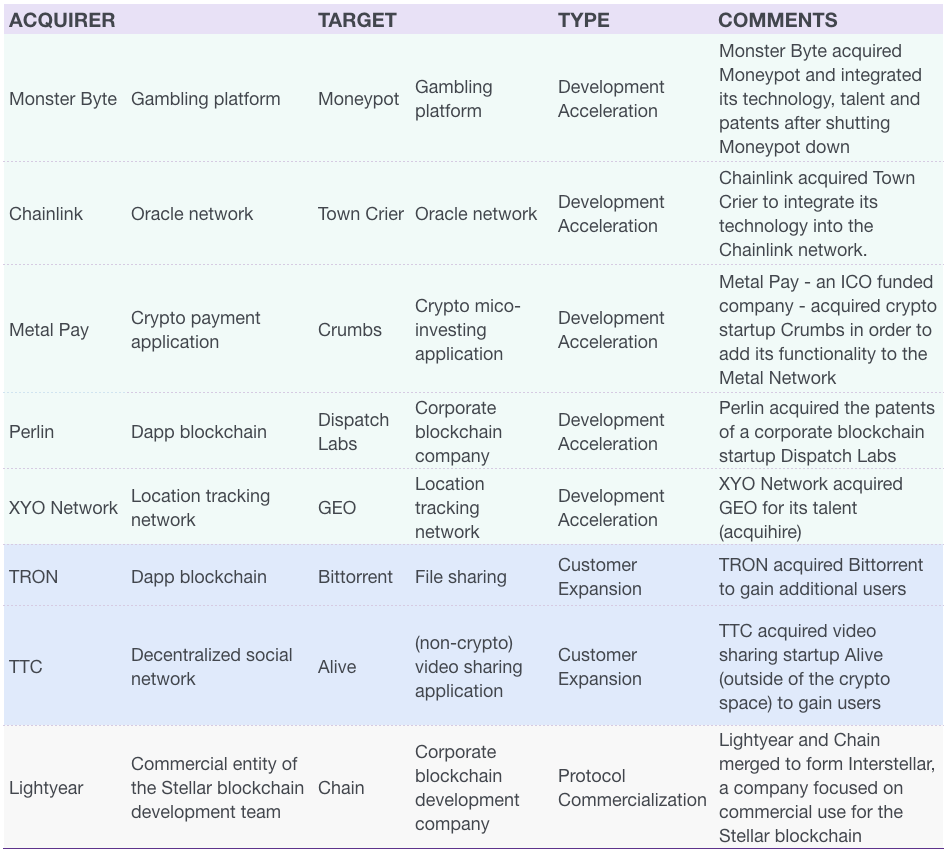

While true “Decentralized M&A” is yet to happen there has been significant M&A activity from the development teams of cryptocurrency networks. Many of these development teams aspire to create a decentralized protocol or application and M&A can be a useful strategic tool as they seek to transition. We have identified 3 different deal types by these teams.

- Development Acceleration: acquisitions by decentralized protocol development teams. Very similar to tuck-in acquisitions these deals are focused on talent (acquihires) and technology. We have seen a few ICO-funded teams engage in this.

- Customer Expansion: acquisitions of non-crypto companies/networks with an existing user-base. Instead of growing a user-base organically, new users are acquired and have to start using the cryptocurrency network and/or tokens.

- Protocol Commercialization: acquisitions by development teams with the ultimate goal to commercialize their open source cryptocurrency protocol. For example, Lightyear – an entity formed by the Stellar development team – merged with Chain – a corporate blockchain company. The merged company was rebranded as “Interstellar” and brings Chain’s customers to the Stellar blockchain.

The first token mergers

2019 saw the first cases of token mergers. After the ICO and token-sale hype of 2017 it was a matter of time until overfunded crypto projects would struggle with traction and look to merge with one another. We found two examples:

- TRONAce & TRONDice: In April 2019, two gambling applications running on the TRON blockchain each with their own token announced that TRONAce had acquired TRONDice and that TRONDice tokens would be merged/swapped into TRONAce tokens.

- COSS & ARAX (a.k.a LALA): In April 2019, Singapore-based crypto exchange COSS and crypto wallet ARAX announced they would merge. Both companies had raised funds in 2017 through ICOs issuing utility tokens. Post merger, the projects’ token holders have swapped the original tokens to a new token representing the merged entity.

Although both mergers weren’t strictly speaking “decentralized” as the projects involved were traditional companies, they are relevant from a token perspective.

A detailed look at the COSS-ARAX token merger can be found in the full report:

Enter email to receive a link to download the full report

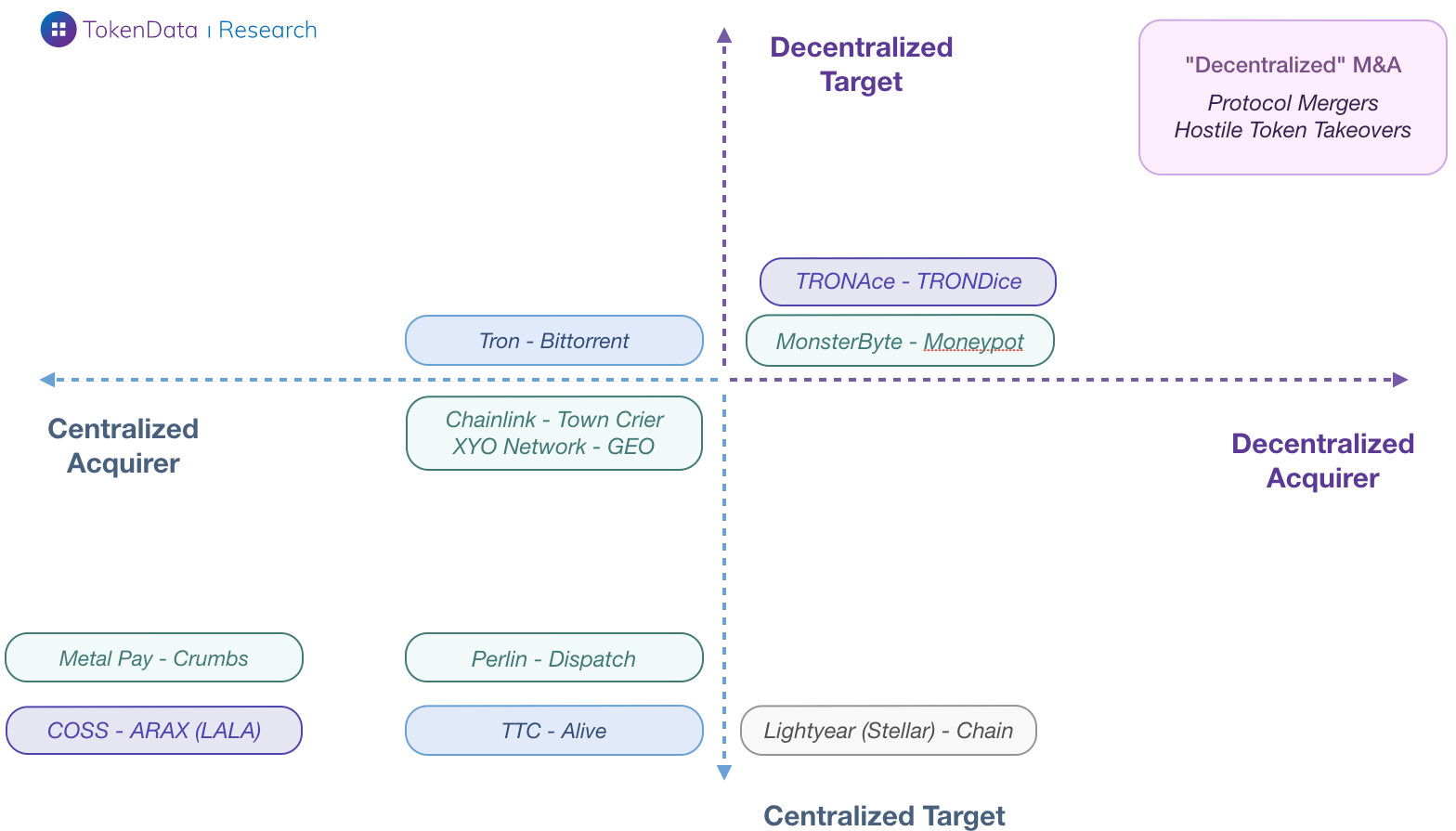

Mapping deals in a centralized-decentralized matrix

This graphic illustrates where the mergers and acquisitions involving protocol and dapp development teams sit on a centralized-decentralized matrix (for both acquirer and target). Since there is no objective measure, the scale is only relative, e.g. we placed the TRONAce – TRONDice merger in the top right quadrant because it involves two dapps and the mechanism used was a token merger. In comparison while COSS – ARAX (LALA) also used a token merger mechanism, the two entities were highly centralized. In the top-right is the hypothetical case of Decentralized M&A where both entity and mechanism fit squarely in the decentralized camp. We leave it to the readers to consider whether the rubicon of decentralization has been crossed, and feedback is welcome!

Key Takeaways

To summarize, we have analyzed 350 deals from 2013-2019 in order to understand what role M&A plays within the cryptocurrency industry. Looking to the future we have considered what “Decentralized M&A” could look like, and assessed transactions that provide clues.

Industry Maturity The cryptocurrency industry hasn’t been shy to engage in M&A. 350 acquisitions have taken place since 2013, representing $4B of value. Whilst meaningful within the industry, both activity and value are relatively small compared to the public valuation of cryptocurrency networks and M&A in other tech sectors. The cryptocurrency space is still relatively young, and M&A activity is a reflection of crypto companies iterating and using acquisitions as a strategic tool.

Volatility M&A activity is volatile and shows signs of positive correlation with cryptocurrency prices. The extreme price run-up in late 2017 drove a surge in sometimes opportunistic Financial M&A. The subsequent price collapse and recovery have created a climate in which Strategic M&A prevails.

Funding Most cryptocurrency companies are funded by venture capital firms. In the absence of a large IPO in the foreseeable future, and the young vintages of most crypto VCs, M&A is not a fund-returning exit strategy yet.

Companies & Strategy Cryptocurrency exchanges such as Coinbase and Kraken have emerged as the most prolific strategic acquirers in the space. Acquihires (talent) and technology focused acquisitions have been the most common strategic type, and we expect this to continue for the foreseeable future.

Regulation There have been clear signs of exchanges using M&A to meet different countries’ regulatory requirements. With the regulatory landscape evolving at high speed, M&A will become an even more attractive strategy for crypto companies in their quest for global regulatory compliance.

Decentralization True “Decentralized” M&A has not happened yet. However, development teams have been actively acquiring companies to help them transition from a centralized starting point to a more decentralized end-state. Moreover, 2019 saw the rise of token mergers, which could be an important mechanism in Decentralized M&A.